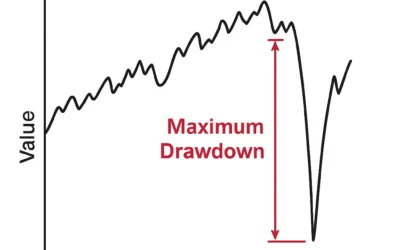

Maximum Drawdown (MDD) is one of the most critical risk metrics for any investor. In this article, we break down what it is, how it works, and how to use it to make smarter investment decisions.

Maximum Drawdown – Your Portfolio’s Pain Threshold

read more